Hey, have you seen that chart floating around about Nvidia? The one that’s got everyone buzzing ahead of its big earnings drop on February 26, 2025? If not, buckle up—because it’s a doozy. Nvidia, the chip giant powering the AI revolution, is trading at a valuation that raises eyebrows. Yahoo Finance tossed out a mind-bender: it’s among the cheapest AI stocks. Yeah, you read that right—cheap. With earnings just days away, let’s dive into what this chart means, why it’s got Wall Street chattering, and what it could spell for your next move—whether you’re an investor, a tech geek, or just here for the drama.

The Chart That’s Turning Heads

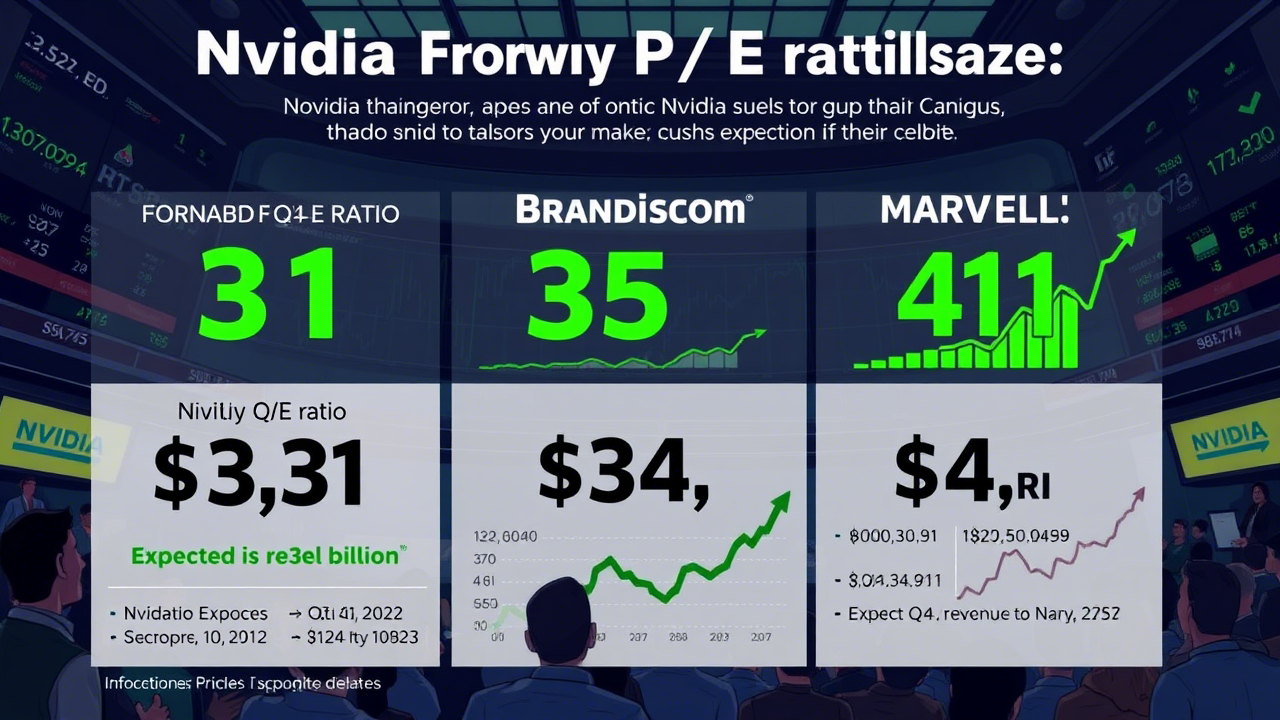

Picture this: a simple graph comparing Nvidia’s forward price-to-earnings (P/E) ratio to other AI heavy hitters. Yahoo Finance crunched the numbers, and here’s the kicker—Nvidia’s sitting at 31 times its forward earnings. Compare that to Broadcom at 35 times or Marvell Technology at 41 times, and suddenly, Nvidia looks like the bargain bin pick of the AI bunch. I stumbled across this on Sunday morning, sipping coffee, and nearly spit it out. Nvidia—the stock that’s been a rocket ship for years—cheap? Really?

The article’s take? Wall Street might be underestimating Nvidia’s earnings power. Analysts have trimmed their first-quarter earnings-per-share (EPS) forecasts over the past month, but this chart screams, “Hold up—there’s more to the story.” With Nvidia’s stock hovering near all-time highs (it’s danced around $140 lately, per recent X posts), this valuation twist is either a golden opportunity or a head-scratcher. Let’s break it down.

Nvidia’s Story So Far

If you’ve been anywhere near a stock ticker in the last few years, you know Nvidia’s been the belle of the AI ball. In 2022, when OpenAI’s ChatGPT lit up the world, Nvidia’s chips—the GPUs that power AI models—became the hottest ticket in tech. I remember my small-time investor cousin jumping in after Nvidia’s blowout earnings in May 2023. “It’s like printing money,” he said, grinning as the stock soared past $100. He wasn’t wrong—Nvidia’s revenue tripled in a year, hitting $26 billion by Q1 2024, fueled by data center demand.

But 2025’s been a bumpier ride. The stock dipped 21% earlier this year when China’s DeepSeek AI startup shook the market with a cheap rival model—proof not everyone needs Nvidia’s pricey chips. It’s clawed back most of that loss, but the shine’s dulled a bit. Now, with earnings looming, this chart’s hinting at a plot twist: maybe Nvidia’s still got room to run.

Why the ‘Cheap’ Label Fits (Sort Of)

Let’s unpack that P/E number—31 times forward earnings. In a vacuum, that’s not cheap; it’s pricier than the S&P 500’s average of 23. But zoom in on AI stocks, and it’s a steal compared to peers betting big on the same tech wave. Broadcom’s riding its own AI boom, and Marvell’s pitching custom chips, yet Nvidia’s outpacing them in raw revenue—$38.13 billion expected for Q4, per LSEG estimates—still looks undervalued.

Here’s the catch: Wall Street’s EPS guesses ($0.85 for Q4) might be lowballing it. Nvidia has a habit of smashing expectations—think 20% beats like clockwork since ChatGPT dropped. I chatted with my buddy Mike, a financial analyst, about this over beers last night. “The Street’s cautious because of DeepSeek and export curbs to China,” he said, “but Nvidia’s ecosystem—CUDA software, hyperscaler deals—it’s a fortress.” If he’s right, that “cheap” tag might hold water.

The Stakes for February 26

Earnings day isn’t just a report card—it’s a crystal ball. Investors want a big beat (say, $40 billion in revenue) and a rosy outlook for 2026. Why? According to their latest calls, giants like Amazon and Meta are pouring billions into AI infrastructure—$75 billion and $40 billion in 2025 capex, respectively. Nvidia’s chips are the backbone of that buildout. “It’s not just about now,” Russell Investments’ Kate El-Hillow told Yahoo Finance. “AI’s a decades-long play.”

But there’s pressure. A modest beat won’t cut it—Nvidia needs a knockout to justify its $3 trillion market cap (second only to Apple). Any whiff of slowing growth—or worse, supply chain snags with its new Blackwell chips—could tank the stock by 7%, as Wall Street bets suggest. My cousin’s already sweating it. “I’m holding,” he texted me yesterday, “but man, this better be good.”

Real-Life Ripple Effects

This isn’t just Wall Street noise—it hits the ground, too. Take Sarah, a startup founder I met at last month’s tech meeting. Her AI-driven health app relies on Nvidia GPUs. “If prices drop or supply tightens, we’re toast,” she said. A strong earnings report could mean more chips and lower costs—good news for her team. Then there’s Jake, a gamer buddy waiting on Nvidia’s next-gen cards. “I just want a damn RTX 5090,” he grumbled. Earnings could signal whether Nvidia’s prioritizing AI over gaming again.

Even if you’re not in tech, it matters. Nvidia’s moves sway markets—think Dow dips or Nasdaq surges. A stumble could spook investors jittery about 2025’s economic wobbles (consumer confidence just hit a 15-month low, per Yahoo Finance).

Expert Takes: Bull vs. Bear

The pros are split. UBS is bullish, predicting Nvidia’s Blackwell chips will ramp up in March 2025, driving a revenue spike. “They’ll exceed expectations,” their analysts told Yahoo Finance, citing hyperscaler demand. KeyBanc’s even bolder—$190 price target, calling Nvidia’s two-year growth “spectacular.” They see 10-12 million GPUs shipped as AI computing doubles.

But bears growl, too. JPMorgan’s Kerry Craig warned CNBC that Nvidia’s 70%+ gross margins might not last—competition’s heating up. While chatting on Yahoo Finance’s Opening Bid, Bill Gates said, “Others are catching up.” DeepSeek’s $6 million model rattled the cage—could cheaper rivals chip away at Nvidia’s throne?

Why This Chart’s ‘Ridiculous’

Here’s the rub: calling Nvidia “cheap” feels absurd when it’s a $3 trillion titan. That’s the chart’s genius—it flips the script. Most stocks at 31x earnings scream overpriced, but Nvidia’s growth—73% revenue jumps year-over-year—makes it a unicorn. Still, I can’t shake the feeling it’s a stretch. My analyst pal Mike shrugged, “It’s only cheap if they keep delivering miracles.”

Posts on X echo that tension. One trader mused, “$NVDA rejected at all-time highs—earnings better break that trendline.” Another quipped, “Cheap? Tell that to my wallet after buying at $120.” The chart’s a conversation starter, not a gospel.

What’s Next for Nvidia?

Post-earnings, it’s go big or go home. A blowout—say, $42 billion and upbeat guidance—could push Nvidia past $150, maybe $190 like KeyBanc Dreamer X chatter, A miss, or tepid 2026 vibes, is back to the $126 support level. In the long term, the AI boom’s real—$1 trillion markets in accelerated compute and generative AI, per analysts—but Nvidia has to dodge China bans, rivals, and its sky-high bar.

For now, I’m watching with popcorn. This chart is a teaser, but the earnings are the main event. Whether you’re rooting for Nvidia or love a good show, February 26’s gonna be wild.

FAQs About Nvidia’s Earnings and That Chart

What’s the ‘Ridiculous Chart’ About?

It’s a Yahoo Finance gem showing Nvidia’s forward P/E at 31x—lower than Broadcom (35x) and Marvell (41x)—suggesting Nvidia’s a bargain among AI stocks despite its massive size.

When Are Nvidia’s Earnings?

February 26, 2025, after the market closes. Wall Street expects $38.13 billion in revenue and $0.85 EPS.

Why Might Nvidia Look Cheap?

Its growth outpaces peers—73% revenue increase expected—and analysts think forecasts are too low. Plus, its CUDA software keeps it king of AI chips.

Could Nvidia Disappoint?

Sure. Supply hiccups with Blackwell chips, softer guidance, or DeepSeek’s rise could spook investors. A 7% stock swing’s in play either way.

Should I Buy Before Earnings?

Risky call—it depends on your gut. Bulls see a breakout; bears smell a trap. Historically, Nvidia beats big, but this time, expectations are sky-high.